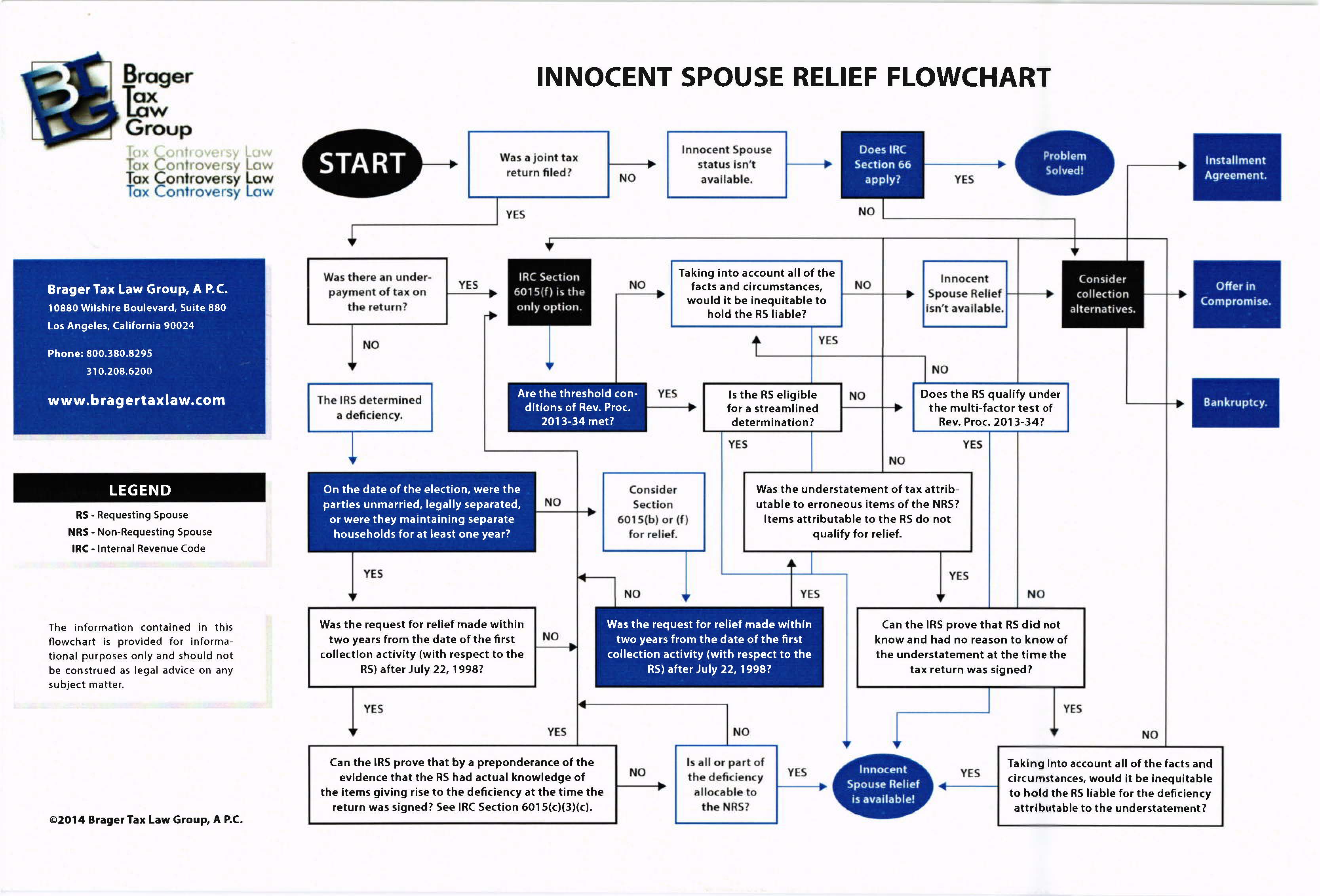

In IRS Notice IR 2012-3 the IRS announced that innocent spouse defenses pursuant to IRC Section 6015(f) will become a little easier. Generally there are three different kinds of innocent spouse defenses, each with its own rules and exceptions. IRS Notice 2012-8, which somewhat confusingly was announced in IRS Notice IR 2012-3, sets out a proposed new Revenue Procedure which will supersede Revenue Procedure (Rev. Proc.) 2003-61. IRS Notice 20012-8 addresses the criteria used in making innocent spouse relief determinations under the equitable relief criteria of Internal Revenue Code Section 6015(f). The IRS Notice covers several topics. It provides for certain streamlined determinations; it creates new guidance on the potential impact of economic hardship, and the weight to be accorded to certain facts in determining equitable innocent spouse relief. Importantly it also expands how the IRS takes into account abuse and financial control by the nonrequesting spouse in deciding whether to grant equitable relief.

The IRS is inviting comments on the forthcoming proposed Revenue Procedure. The comments must be submitted by February 21, 2012.

One important change is that under Rev. Procedure 2003-61, which previously provided guidelines for equitable innocent spouse determinations, lack of economic hardship was treated as a factor which weighed against granting equitable innocent spouse relief. Now if economic hardship exists that is still a factor which weighs in favor of granting innocent spouse relief. However, the lack of economic hardship will no longer be counted against a requesting spouse. Instead it will be treated as neutral.

Another significant change is that the proposed revenue procedure provides that abuse or lack of financial control may mitigate other factors that might weigh against granting equitable relief under IRC Section 6015(f). For example, even though a requesting innocent spouse has knowledge or reason to know of omitted income on a tax return if the nonrequesting spouse abused the requesting spouse or maintained control over the household finances by restricting the requesting spouse’s access to financial information, and, therefore, because of the abuse or financial control the requesting spouse was not able to challenge the treatment of any items on the joint return for fear of the nonrequesting spouse’s retaliation, then that abuse or financial control will result in this factor weighing in favor of relief even if the requesting spouse had knowledge or reason to know of the items giving rise to the understatement or deficiency.

In the end, however, the granting of innocent spouse relief is based upon all of the facts and circumstances. Only by discussing your case with a knowledgeable tax litigation attorney can you determine if you are likely to prevail.

Continue Reading ›